CARDS

February 26, 2025

5 min to read

- Copy link

- Share on X

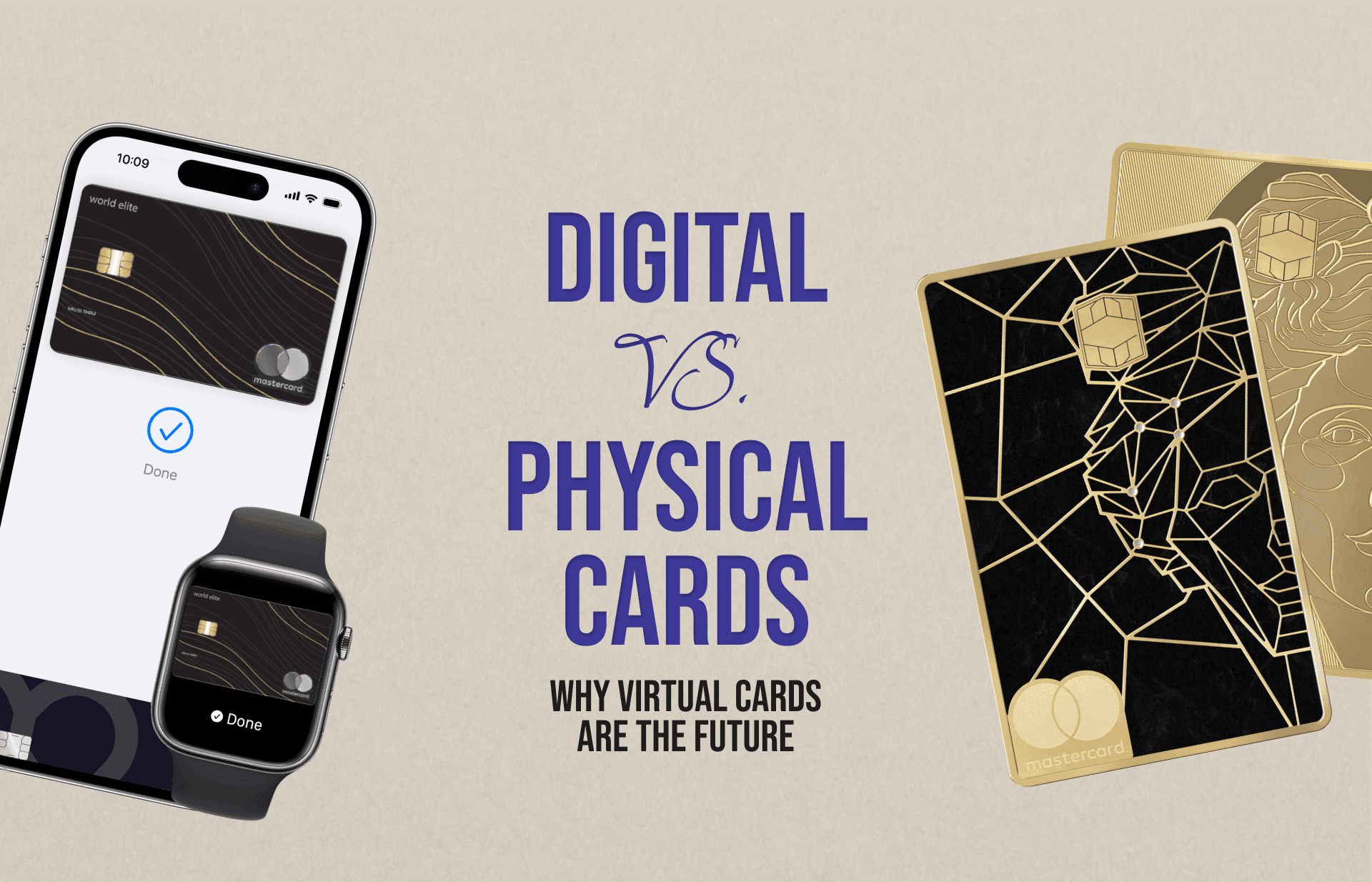

Digital vs. Physical Cards: Why Virtual Cards Are the Future

Virtual card technology has exploded in recent years, with more people than ever enjoying the benefits of virtual cards. The digital vs physical cards debate has become increasingly weighted towards the former, with ongoing innovations allowing for greater efficiency, security and flexibility of payments. It is forecast that virtual cards are averaging at over 35 billion transactions a year, with the market to grow by 30% by 2028. However, if you’re new to this innovative new payment form, here is everything you need to know about the advantages of virtual cards.

How virtual cards work

As the name suggests, virtual cards – unlike physical cards – exist entirely in the digital realm. These often serve as counterparts to traditional debt, credit and prepaid cards issued by financial institutions. Users can link a virtual card with their existing bank account, enabling seamless integration between the physical and virtual forms. These can still be used in the same way, from making retail payments to withdrawing cash from cash machines.

Virtual card technology is easily explained. Imagine you go to your local café to buy a coffee – by using a virtual card, the café sends an approved payment file to the virtual card provider (usually a financial institution). The card provider generates a unique 16-digit virtual card number for the payment amount, which is then sent to the payee on behalf of the company and often through a secure message. Once authorised, the payee’s bank and company’s bank settle the transaction. The payment posts on the company’s account, and a reconciliation file is automatically sent to the company’s Enterprise Resource Planning system to match bills.

This all takes seconds! Furthermore, a unique 16-digit virtual card number is generated for each individual transaction which heightens security and minimises fraud risk.

Why virtual cards are the future

One of the main advantages these virtual cards have, over physical cards, is the security features they bring users. A major disadvantage to physical cards is these can be stolen, and credit card fraud is still a multi-billion pound criminal industry. Physical cards can be physically lifted from a person’s pocket or wallet, or the information can be spotted from their surface. Although banks and payment providers alike offer customers the ability to quickly freeze cards if they’ve been stolen, sometimes the damage has already been done.

Therefore, the enhanced security with virtual cards is a clear win for users. You can use a virtual card without exposing your account number or other sensitive information. Furthermore, virtual cards easily lend themselves to biometric authentication and multi-factor authentication.

The convenience of virtual cards

Virtual cards are the latest, and most exciting, step in the ongoing evolution of payments processing. Cheques were invented as a more secure and convenient way of making payments. Then, payment cards followed as an easier way of making payments than with a cheque. In recent years, contactless and mobile payments have taken things a step further in the pursuit of even greater convenience

Now, you don’t even need a physical card, and virtual cards are set to further transform the space. These are also easier to access and virtual card platforms – granted you pass the security cards – can facilitate instant card issuance with virtual cards. This means virtual cards and make payments, online and in person, even more effortless with little to no friction in each transaction (while not compromising on security).

The way in which virtual cards are created and used means they lend themselves to business use. Instead of a corporate having to authorise and issue physical expenses cards, often overseeing the costs of these (including production and postage), virtual cards are much easier to issue. For virtual cards for expense management, these can also be created with spending limits. The flexibility of virtual cards as solutions for online transactions means these can also be created with appropriate spending limits. By customising the spending and transaction limits for each virtual card, individuals can ensure that expenses related to projects, events, and departments align with the allocated budgets. This tailored approach provides a clear overview of the available funds for each specific use, ultimately mitigating the risk of overspending.

The future of virtual cards

Like with all modern innovations, virtual cards are being met with a mixture of excitement and trepidation. The latter means some will be wary of this technology and prefer having a physical card in their hands, with these also the kind of people who prefer physical cash.

However, like with contactless and other payment innovations, use of virtual cards will lead to greater adoption as people see first-hand how these work and the flexibility and greater security they can give people. This is an exciting time in payments, and we can’t wait to see where innovations like virtual cards take the industry next!

To get more insights from the Cardaq team as they’re published, sign up to a newsletter below:

Don’t miss out on fintech insights, company milestones, and expert tips

Subscribe now to stay ahead in the fintech world!

- WEB

- ALGORITHMS

Can You Go a Week Without Algorithms?

- FINTECH

- MEME

What If Your Bank Was a Meme Page?

- FINTECH

- STARTUPS

Biggest FinTech fails and what startups can learn

- STORIES

- FINTECH

Fintech Horror Stories: When automation goes wrong

- BANKING

- GUIDE